Personal Services Income and Service Entity Arrangements

Manager at LDB Group

Member of Institute of Chartered Accountants Australia and New Zealand

Adam together with a supportive team, manages a diverse portfolio of clients across a range of sectors including medical practices, allied health professionals, information technology, lawyers, real estate and private family groups.

Adam has experience in transitioning medical professionals looking to transition from employment to setting up their business. Adam understands the challenges to starting up a business, so works closely with his clients to keep things simple and provide all of the support needed to allow his clients to do what they do best. As part of his engagements with clients, Adam will help identify the cash flow issues arising when setting up a business, ensure that clients remain compliant with their obligations and will be there every step of the way as their business grows.

This experience allows Adam and the team at LDB to have a broad range of knowledge across the various accounting and taxation issues faced in multiple industries including the medical industry. This experience puts LDB in a position to provide excellent advice and client support and service for all client industries.

About LDB

![]() Our team of specialists at LDB work as one to deliver personal friendly service and real results at every stage of your business and your personal affairs. We offer a full suite of services being accounting advisory, superannuation, wealth management, audit, tax consulting, lending & financing, owners’ corporation management and property consulting & management.

Our team of specialists at LDB work as one to deliver personal friendly service and real results at every stage of your business and your personal affairs. We offer a full suite of services being accounting advisory, superannuation, wealth management, audit, tax consulting, lending & financing, owners’ corporation management and property consulting & management.

The team that specialises in the health sector understands and appreciates all of the challenges when setting up and managing your business. We take great pride in offering our clients in this sector a tailored solution including but not limited to tax planning and structuring, GST, registrations and insurance, cash flow, Medicare and private health insurance management, the right structure from being an employee through to being a corporate entity in business, also succession planning.

If you have any questions or wish to talk about anything that LDB might be able to assist with, please contact Adam Betts on 03 9875 2900.

How LDB can help?

Decisions when setting up a private practice and deciding on the most appropriate structure for your business can be hard to make. It is important to remember that some of the above challenges can be managed and mitigated with the right support and advice.

The accounting and tax team at LDB Group can help you with the getting the right structure for you for asset protection and put in place strategies to help streamline all of your accounting needs.

Our financial planners can help you get the right income protection and other personal insurances in place to lessen the impact of any lost income if you are ever injured or ill and physically unable to work.

Introduction

Following our article in Volume 22, Number 1 published in February 2019 (Personal Services Income and Service Entity Arrangements) and our presentation at the Australasian Diabetes Congress Sydney 2019, we wanted to explore further the topic of personal services income, as this is an issue very relevant to the health profession and more specifically Credentialled Diabetes Educators (CDE) working in private practice.

In this edition, we want to take you through some different scenarios where we begin to apply some of the theory and technical information about the Personal Services Income (PSI) regime, as well as going over Service Entity Arrangements.

Personal Services Income (PSI)

We discussed how the PSI flowchart works in previous articles, in our April 2019 webinar series and at ADC 2019.

Although the PSI tests may potentially be satisfied when working through the questions, we touched on the fact that the additional legal protection and limited liability offered under a corporate structure (or other structures) in most cases are not tax effective for medical practitioners, where any protection and liability failings will be at a professional level. Therefore, the PSI tests and exploring options to split client/professional income would not apply and if done would fall afoul of Part IVA (income tax anti-avoidance provisions). So, in conclusion, we will not be able to rely on PSI to be able to have income attributable to beneficiaries other than the CDE. In other words, any income earned from seeing clients must be taxed as personal income.

So, what does this all mean for a CDE?

How can we then argue that we are generating profits for personal exertion in an entity other than the person performing this task? In most situations we cannot and therefore PSI and the associated tests become relatively redundant.

If you are in a scenario where you need to consider the PSI rules, there is a high chance your structure is at risk of falling afoul of part IVA.

This is another reason to ensure you are getting advice and the correct structure put in place at the start!

Does this mean there are no structuring opportunities for medical professionals? We will explore this next.

Below, we have summarised three different tax scenarios, covering a CDE being a Sole Trader, a CDE working through a Company Structure and then a CDE working with a Service Entity Arrangement in place.

Examples

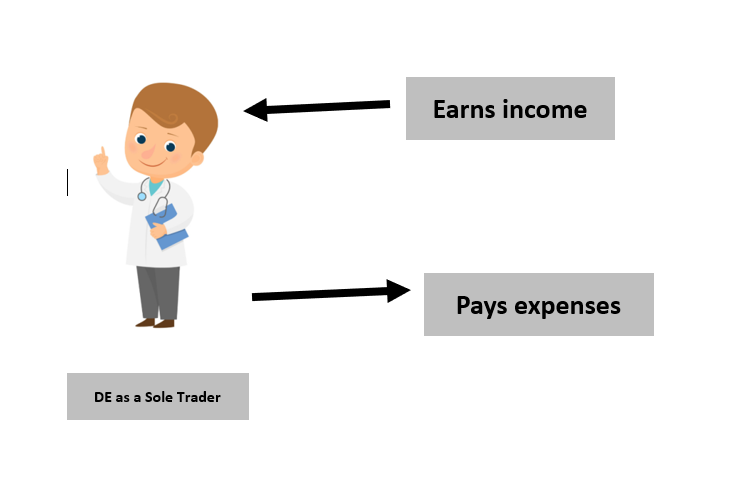

Scenario 1 – CDE working alone as a sole trader (no staff)

For a CDE trading as a Sole Trader, all CDE income and expenses will be reported under their personal ABN.

For a CDE trading as a Sole Trader, all CDE income and expenses will be reported under their personal ABN.

In terms of paying tax, the CDE will pay tax at their marginal rate of tax based on their net profit earned during a financial year.

The net profit from the services provided as a CDE will be reported in the tax return of the CDE along with any other income earned such as interest and dividend income or salary income.

Under this scenario, there is no ability to share profit among to other individuals apart from the CDE.

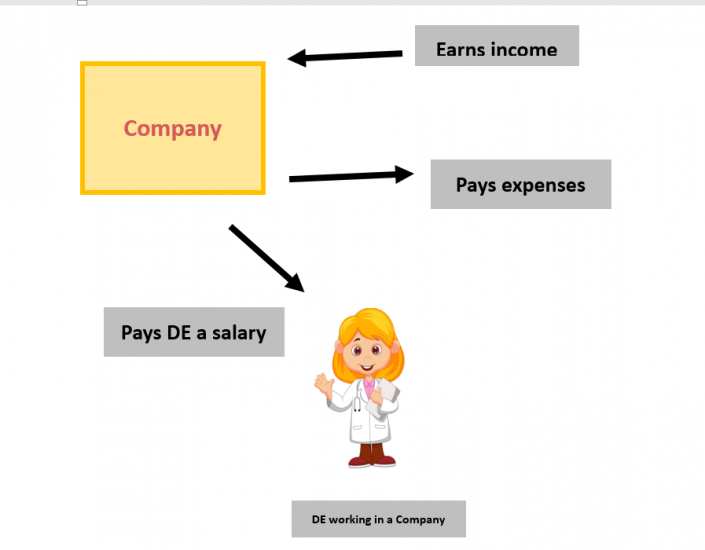

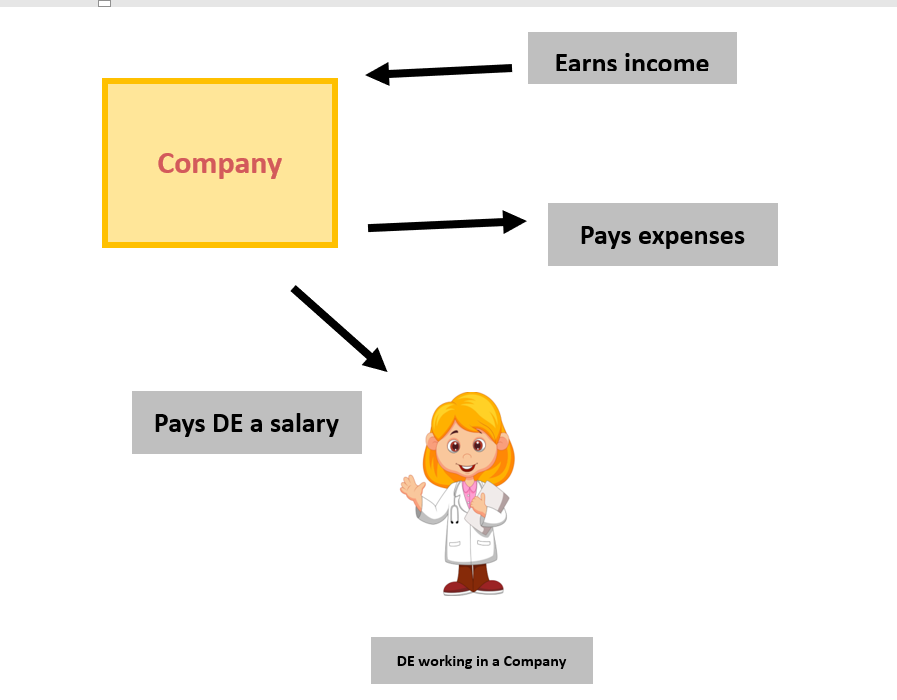

Scenario 2 – CDE working with reception/support staff and company structure, CDE is employee of company

In this example, we have a CDE working as an employee and director of the Company.

The CDE is responsible for providing the client advice/services while working in the Company.

Income is being earned within the Company, with expenses being paid such as wages to employees (support staff/reception), rent and other professional/business expenses. The CDE is also being paid a salary throughout the financial year.

Now, as the PSI rules do not apply, we are not able to keep any remaining profits in the Company to be taxed at the current Company tax rate of 27.50%.

Because of the PSI and splitting rules detailed in Tax Ruling 2330, the remaining profits in the Company must be attributed back to the CDE and added as additional income to the salary earned during the course of the financial year.

There are steps on how to attribute the remaining PSI – refer to the below link on the ATO website for more information:

https://www.ato.gov.au/Business/Personal-services-income/In-detail/How-to-attribute-PSI/

Similar to scenario 1, there is no way to tax effectively share income earned by the CDE in this Company structure.

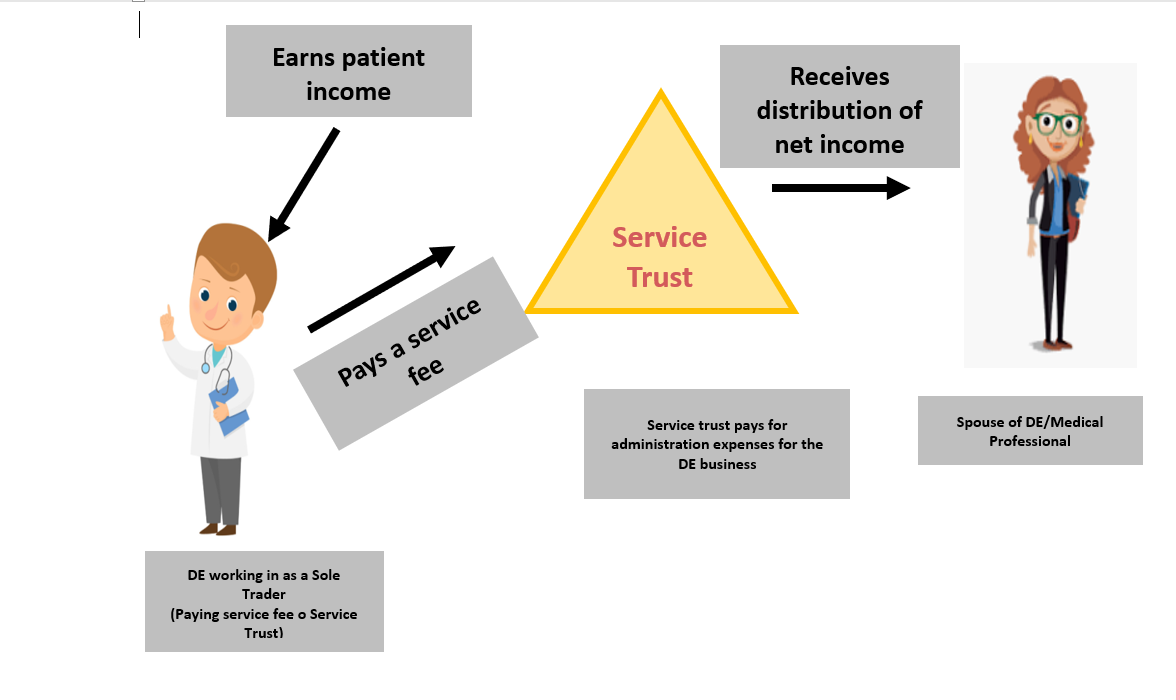

Scenario 3 – DE working with both reception and clinical staff in a service trust structure, DE is a sole trader

In this example, we are now exploring the structuring opportunities for health professionals.

What is a Service Entity Arrangement?

Service Entity Arrangements are covered in Tax Ruling 2006/2.

Service arrangements, in essence, involve a taxpayer (DE) incurring a deduction for service fees and charges in the conduct of its business by using an associated entity such as a company or trust which is controlled by the taxpayer (the service entity).

These fees and charges could be for:

- Acquisition of staff

- Clerical and administrative services

- Premises

- Plant and or equipment

These arrangements are sometimes referred to as Phillips arrangements (this is the case which established the precedent the ATO has to follow).

The decision of the courts in FCoT v Phillips case (1978) was to direct that deductions must be accepted as reasonable by the ATO if it is shown:

- That it is a rearrangement of business affairs for commercial reasons and realistic charges not in excess of commercial rates

- Note there must still be a commercial explanation for the expenditure

It is important when considering using a service entity to ensure an adequate commercial explanation is available. So speaking to a tax advisor with knowledge in the medical industry is very important to ensure you receive the right tailored advice that suits your satiation.

Scenarios where the ATO may view a service arrangement not to have an adequate commercial explanation in some of the following examples:

- The service fees and charges are disproportionate or grossly excessive in relation to the benefits conferred by the service arrangement;

- The service fees and charges guarantee the service entity a certain profit outcome without reasonable commercial explanation; or

- The service fees and charges generate profits in the service entity without any clear evidence that the service entity has added any value or performed any substantive functions. For example, this might occur where there is no clear separation between the service entity’s business activities and those of the taxpayer.

There are multiple benefits of using service arrangements/entities which can include:

- The health professional can focus solely on his or her consultations and outsource the business administration side of the work

- It can be easier for personal management across multiple locations as wages are being paid from one central entity

- It can provide asset protection if another entity holds the real-estate the health professional operates out of

- Provides asset protection for large expensive specialised pieces of equipment

- It may offer tax planning opportunities for the profits generated by these service entities.

In terms of setting a service fee amount, for health practitioners there is a generally accepted rate of up to 30% of the practitioners gross practice fees (up to 45% for rural and sole practitioners). The service fee rate is determined based on arm’s length transactions within the industry, so it is important to review this to ensure you are staying in line with a comparable rate. This rate also assumes a full range of services being offered including premises, so if rent is being paid elsewhere for example, the rate would need to be lowered to reflect this reduction in service. It is also advised that no greater than 30% of combined net profits of the professional and the service entity are earned by the service entity.

Please note there is also an alternative available to use a “mark-up” on expense incurred method, which can be used if desired.

Facts in Scenario 3

So, in this example above, the DE earns client income in their name and the client income is reported under their ABN and tax return (similar to scenario 1).

However they also have a Service Trust in place which pays rent for the building that is being used for their business and other ongoing expenses such as wages for support staff/reception, superannuation and WorkCover for staff, and business running expenses.

The Service Trust charges a service fee using either the comparable rate method (30%) or using a mark-up on actual expenses incurred. The DE then pays this service fee to the Service Trust, which they are able to claim as a tax deduction against the client income reported under their ABN/tax return. The Trust then reports the service fees as income and the net profits (income less expenses in the Trust) can then be legally distributed to the spouse or other beneficiaries of the Service Trust in that financial year. Using the Service Entity Arrangement, assuming this can be put in place after checking that there are no tax avoidance issues in your situation, provides a way to assist in managing the tax of income received in the structure along with other benefits including asset protection.

Conclusion

There is no one entity or vehicle which will always be most appropriate. More often than not, a good structure will include a mix of entities.

The choice of entity must take into account both short term and long term business objectives and consider not only tax issues, but also the non-tax characteristics of each entity.

The health industry is very complex, with the service offerings and revenue often having different tax treatments. One size definitely does not fit all and it is important to chat with an expert such as LDB to ensure you are taking into account all the different issues when setting up your business.